The newly discovered COVID-19 variant known as Omicron spooked the markets last Friday and led to the worst daily performance of 2021, with all major indices down more than 2% amidst a flight-to-quality move across all major assets classes. After a large buy-the-dip rally earlier this week on hopes that the new variant would be less lethal even if more highly transmissible, an early recovery in global markets has given way to some very volatile trading sessions. One of the main culprits is the uncertainty associated with the variant. Biotechnology manufacturer Moderna said it will take some time to figure out how best to deal with and protect against Omicron and that vaccines could be less effective, which the market didn’t react to favorably. Another reason for the downward pressure on stocks is a more hawkish tone from the Fed, which is contemplating a faster-than-expected tapering of its bond buying program (many in the market equate fewer bond purchases with higher rates, all else being equal).

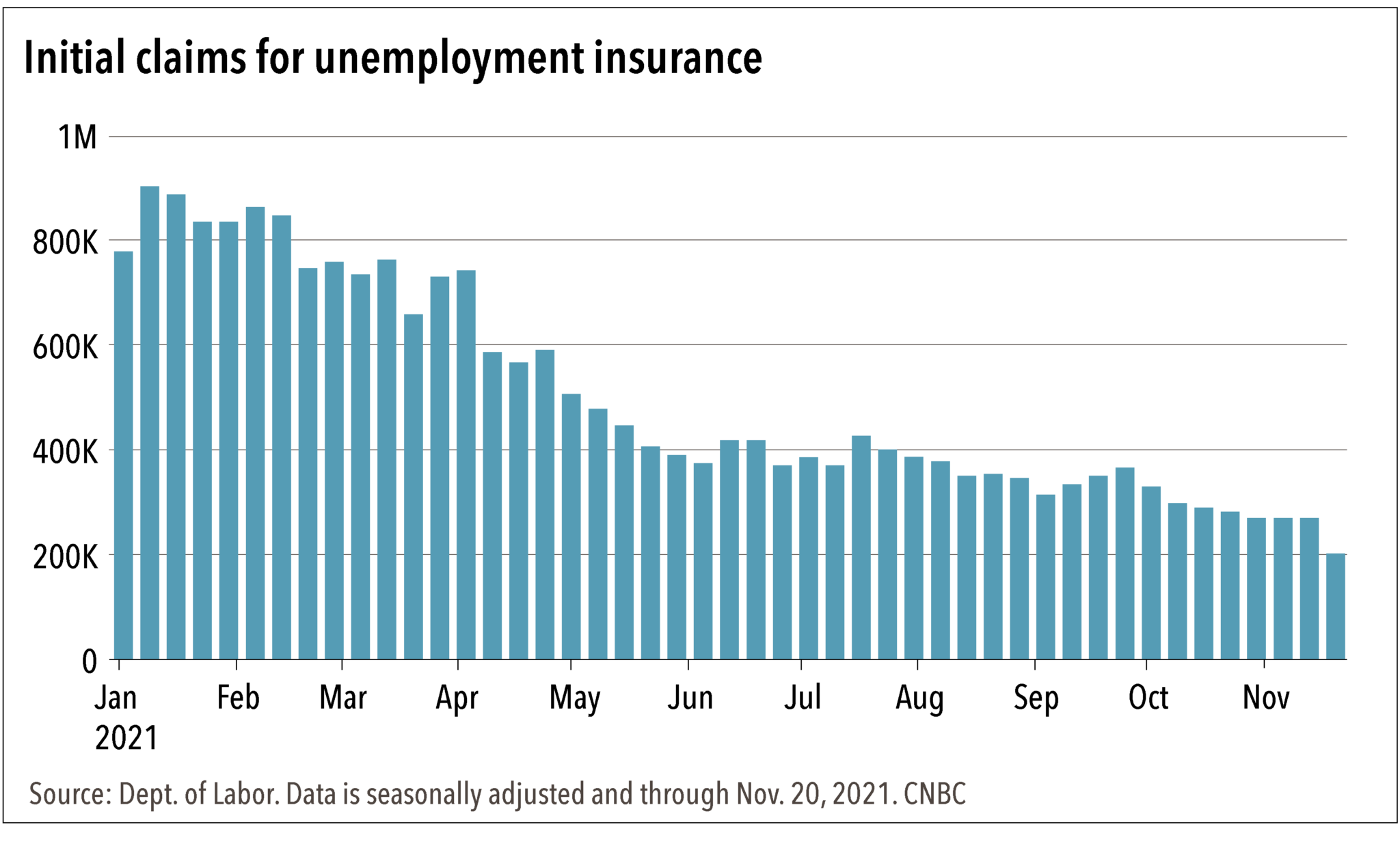

The futures market has quickly priced into the market just two Federal Reserve interest rate hikes next year, down from the three that were previously expected as we went into the Thanksgiving holiday a week ago. With inflation still running high (last week’s core inflation figure was up 4.1% year over year, the highest since 1990), it appears the Fed believes this is a great time to remove some of the easy monetary policies in place since early 2020. Also, with the Fed having a dual mandate for stable prices and maximum employment, it looks more and more like the time is right to hike rates. Initial jobless claims totaled 199K last week, the lowest total since 1969 (see chart below). Given the broad strength of the jobs market, we expect full employment to be reached in Q2/Q3 of next year, right around the end of the Fed’s taper.

However, the Fed has promised not to raise rates until the bond purchasing program is complete. The JNBA Investment Committee believes that quickening the bond taper could be beneficial if the Fed seeks to moderate economic growth more quickly because interest rate adjustments provide them flexibility to address inflation head on. Should 2022 bring faster inflation due to untangling supply chains or Omicron proving to be less of a threat with (or without) an increase in booster shots, the Fed would have freedom to act more quickly, too.

While it seems somewhat rash for the Fed to consider tightening liquidity in the face of bad news, it does provide them with additional credibility on the independence front that they will fight inflation – something more in doubt as of late. And because the futures market has backed off on an extra rate hike, this is considered by investors to be more palatable than before. If the variant proves to be more disruptive and worsens supply chains further, it would likely push up inflation and the Fed might be forced to hike rates anyway, which we would view as appropriate.

Our Investment Committee will be watching closely to see how things develop over the next few weeks and will adjust portfolios as necessary. With the S&P 500 down less than 3% in the last week and smaller stocks down nearly twice that, we believe there is no need for panic and are not surprised that the initial market reaction is “shoot first, ask questions later.” Just as we managed through 2020 using our disciplined investment process that’s been refined over four decades, we’ll continue to manage portfolios prudently with your long-term goals in sight. We believe that for most investors, the market will care less about COVID and more about its indirect impact on the backdrop for inflation, interest rate policies, and corporate earnings – where we’ll keep our focus ahead to 2022.

Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from JNBA Financial Advisors, LLC.

Please see important disclosures information at www.jnba.com/disclosure