We entered 2026 on the heels of another strong year of market performance. Global stocks hovered near all-time highs, the economic backdrop was sound, and investors expected a handful of rate cuts from the Federal Reserve in the year ahead. Even so, concerns lingered about stock valuations and the long-running bull market. Threats are always persistent for investors, some of which were apparent in the early stages of 2026: a disappointing earnings season, cracks showing in the private credit market, and disruption from AI technology advancement. What wasn’t on most investors’ radars was an escalating conflict in Iran that has caused oil prices to surge and have thrown both stock and bond markets into turmoil in short order.

The war in Iran and surging oil prices have dominated headlines and market direction as of late. At their worst, major global stock indexes fell nearly 10%, gold was down over 20% from its all-time high, and bond yields surged to levels not seen since the summer of 2025 – all seemingly showing that there are few places for investors to take shelter – before markets slightly recovered on the last day of the month amid growing optimism towards ending the conflict. As we close out the first quarter of the year with heightened uncertainty and a slew of new variables that complicate the direction of the market, where do we go from here?

In the past, the JNBA Investment Committee has referred to three “pillars” of financial markets or the economy: unemployment, inflation, and corporate earnings. Now, each pillar is facing its own unique set of challenges.

corporate earnings

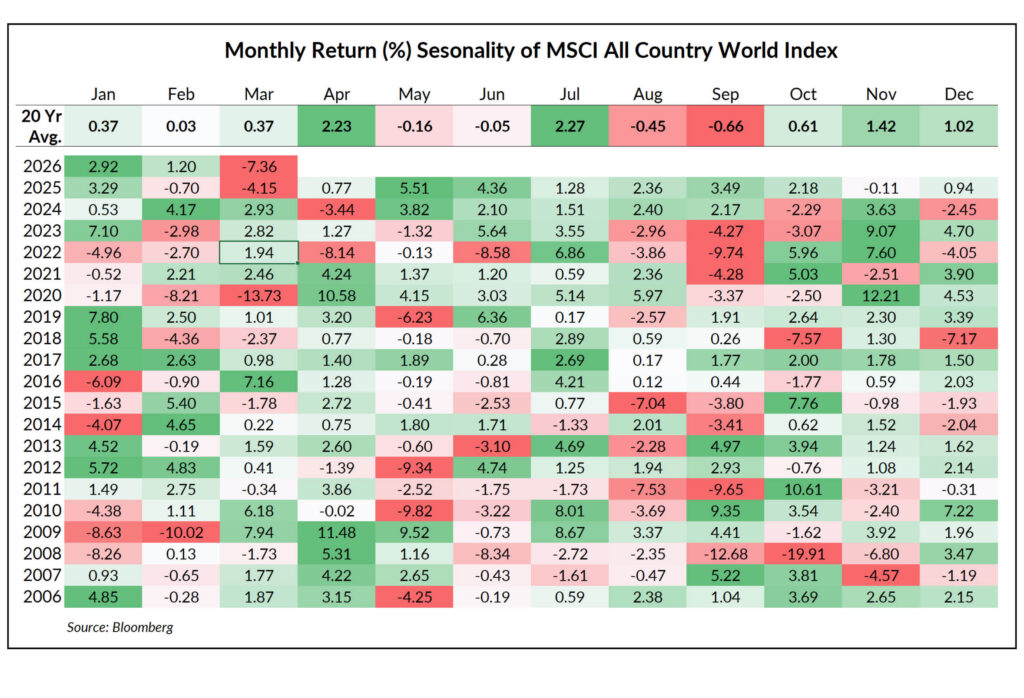

April is historically one of the strongest months of the year for global stocks and also marks the beginning of Q1 2026 earnings season. Q4 2025 earnings proved disappointing for investors as companies struggled to meet expectations tied to elevated valuations, and this past quarter’s results will offer insight into the impact from the war in Iran. Despite the disappointing start to the year from the last earnings season, the S&P 500 is projected to report year-over-year earnings growth of approximately 12.5% for Q1 2026, which would mark the sixth consecutive quarter of double-digit growth and continues to show a healthy backdrop for corporate earnings.

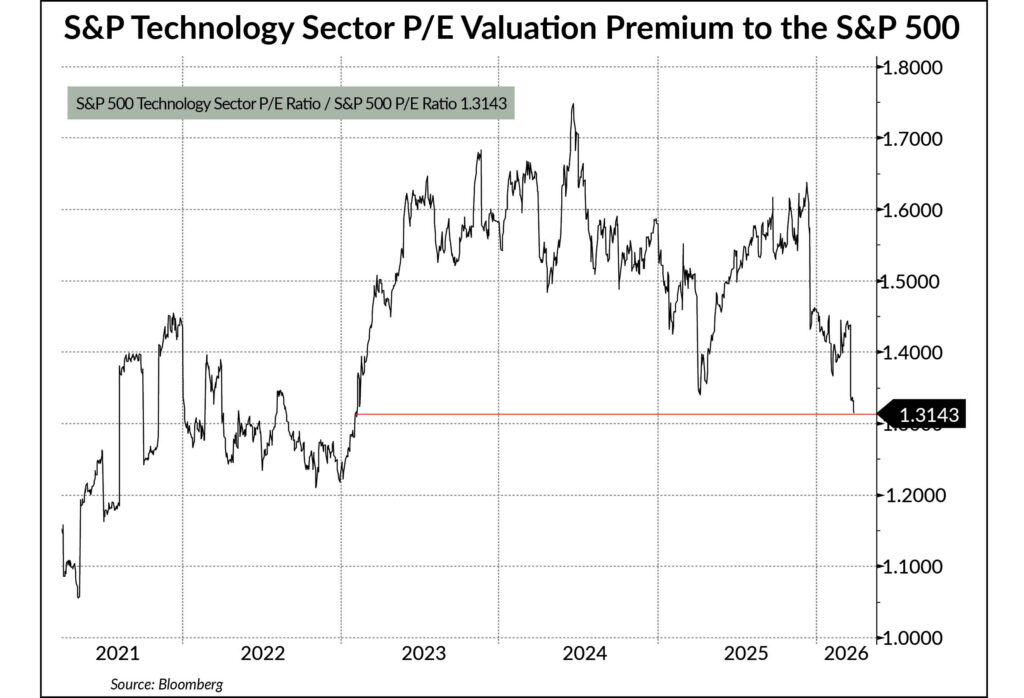

There will eventually be opportunities that arise from this pullback. Technology companies are now trading at the same valuation premium relative to the broader market as they did at the beginning of 2023, the start of the stellar period when the technology sector drove most of the S&P 500’s returns over the past several years. With the recent pullback in prices and valuations, many will wonder if they’re amid an attractive buying opportunity or if geopolitics will continue to dominate headlines and market direction. While we can’t know for certain, the answer also isn’t that simple.

unemployment & inflation

March opened with the release of February employment data, which significantly missed estimates. Economists expected growth in nonfarm payrolls of 55,000 and no change in the unemployment rate, but actual results showed a 92,000 decrease in nonfarm payrolls with the unemployment rate ticking up to 4.4% – raising doubts about the health of the labor market. This was followed by a relatively tame Consumer Price Index (CPI) report that showed continued easing price pressures before the oil and broader economic shock from the conflict in Iran. The second half of March began with a highly anticipated Federal Open Market Committee (FOMC) meeting. Federal Reserve policymakers elected to leave the Federal Funds rate unchanged, and while this decision was largely in line with expectations, the market always looks for clues for what’s next. However, neither the post-meeting statement, the updated economic projections, nor Chair Jerome Powell’s news conference provided much in that regard. As Powell faced repeated questions about the oil shock, he emphasized how much the conflict has muddied the waters for the Fed and underscored how it’s nearly impossible to forecast the future and a modeling policy when the U.S. is at war with Iran. We started 2026 with money markets pricing in at least two rate cuts this year, but after the latest FOMC meeting, money markets are no longer pricing in any rate cuts. Meanwhile, the odds of a rate hike this year are increasing along with the fear of a resurgence in inflation.

Financial markets closed out the quarter on a positive note with a rally across all asset classes on the last day of March, as optimism for a resolution to the conflict in the Middle East in the near future continues to grow following recent comments from both the U.S. and Iran. With the geopolitical environment continuing to be very fluid on a day-by-day basis, uncertainty will remain for the foreseeable future until a formal deescalation of the conflict is observed. Stocks and bonds both remain in a sensitive spot amidst the repercussions from the war in Iran and a backdrop of challenging economic and inflationary data. With the heightened uncertainty becoming more apparent in March, JNBA made a strategic move to position portfolios more cautiously towards stocks.

As your advocate, the JNBA Investment Committee continues to monitor the market environment diligently, remains committed to keeping you informed, and emphasizes the importance of discipline with long-term decision-making through periods of challenging market performance.

We encourage you to reach out to your JNBA Advisory Team with any questions.

Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from JNBA Financial Advisors, LLC.

Please see important disclosure information at jnba.com/disclosure