February 2026 was another month when it was beneficial to be a diversified investor. Market anxiety surged, driving the S&P 500 to its worst month since March 2025 as February was filled with headlines warning that AI could disrupt various industries or even be the demise of certain companies. On the contrary, mid-cap and small-cap stocks each delivered healthy returns – and international stocks returned over 6%, continuing their streak of outperforming U.S. stocks. Not too long ago, it seemed as if U.S. Large-Cap stocks were investors’ main source of returns, and any company with a tether to the AI-theme saw their stock price increasing exponentially. Now, however, we’re seeing indiscriminate selling of companies viewed as highly exposed to disruption from the advancement of AI technology. The vulnerability mainly lies with software companies, but the fear has spread to banking, wealth management, logistics, and even cybersecurity. What was once a main driver of U.S. stock performance now appears to be perceived as a threat. Looking forward, investors must parse through additional risks stemming from the war with Iran and escalating conflict across the Middle East, serving as the next test for financial markets.

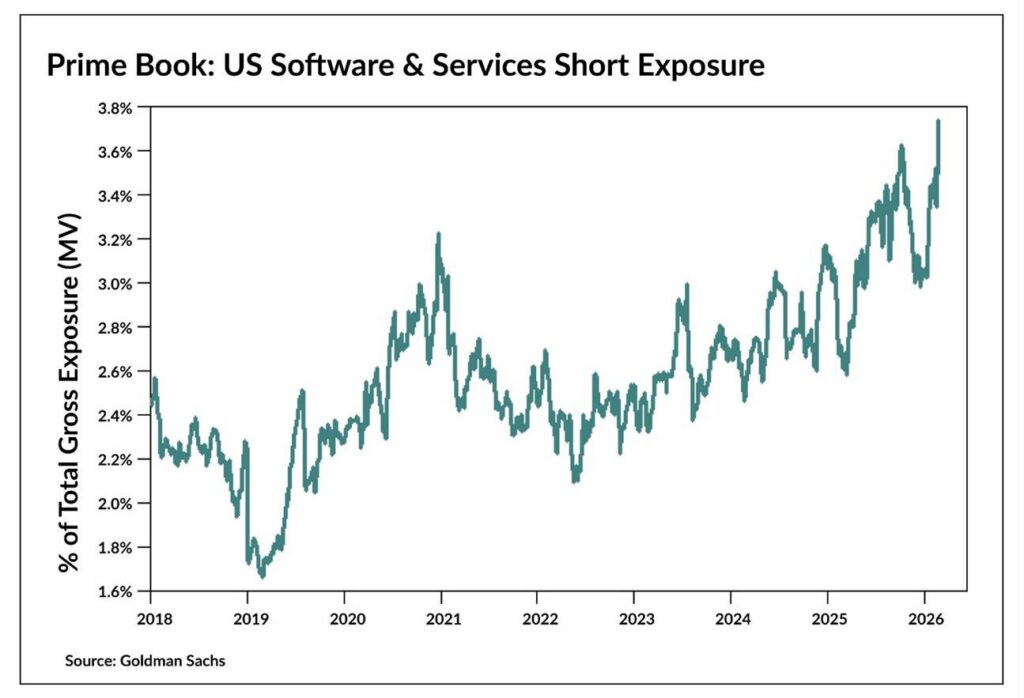

As of Friday’s close (Feb. 27, 2026), the S&P 500 finished the month down just shy of 1% – the worst monthly performance for the index since March 2025 as the “AI Scare” trade took hold. Despite investor concerns over AI disruption, we have continued to see a broadening rally with Mid- and Small-Cap companies outperforming their U.S. Large-Cap counterparts which generated most of the returns the past several years. As you look further, returns aren’t as muted across the board: Software stocks have now lost over 30% of their value since their September 2025 highs, and lost another 10% in February 2026 alone, bearing the brunt of investor angst. Value stocks and others, such as consumer staples and heavy-industry firms, have benefited as they’re viewed as less vulnerable to disruption. Investors increasingly believe these vulnerable sectors face more downside ahead, as short positions on software and services companies have now reached the highest level on record.

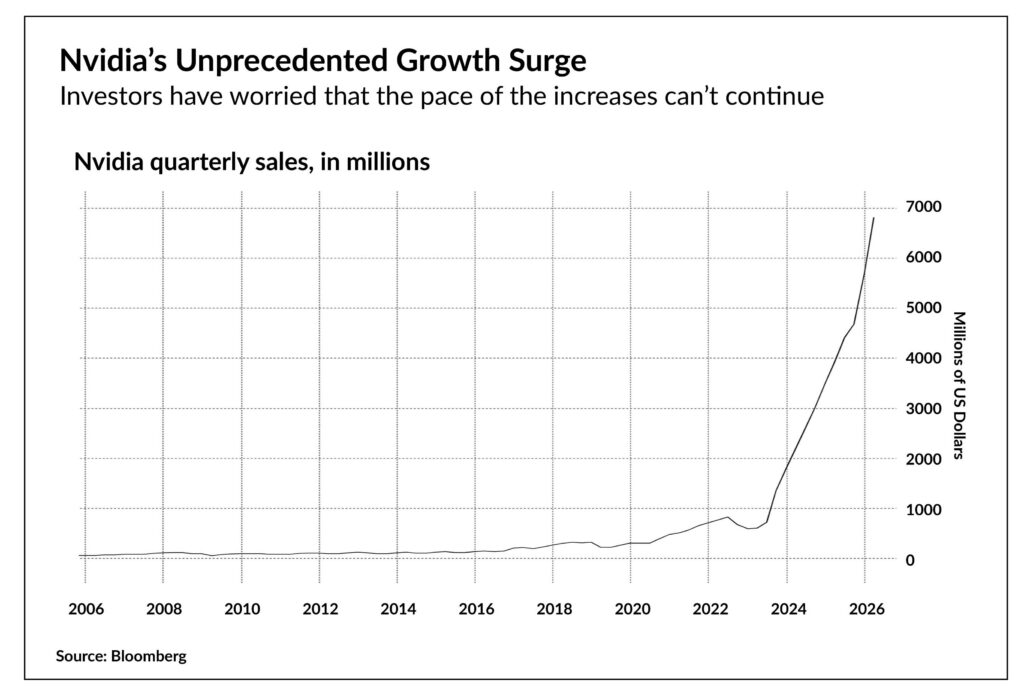

Even Nvidia, the dominant maker of artificial intelligence chips, isn’t isolated from the market’s fears. Nvidia easily beat analyst estimates, delivering a 73% surge in Q4 revenue, and provided an impressive first-quarter sales outlook after reporting Q4 results the last week of February. All of this still failed to dispel fears of an AI bubble, leading to the stock’s worst decline in 10 months as investors seek stronger assurance that booming AI spending can be maintained and can sustain growth beyond just the next few years.

AI disruption fears have spread further than just the public stock market. Private credit has been back in the spotlight this month, with fears growing from the industry’s exposure to software and other vulnerable names. Blue Owl Capital Inc. has permanently halted withdrawals on one of its funds, preventing investors from withdrawing cash, and began selling assets to return investor capital – the latest sign of tumult in a $1.8 trillion market stricken with worry about overspending on artificial intelligence and its disruptive power. Blue Owl shares have tumbled, dragging the stocks of other money managers with it, as some estimates suggest upwards of 40% of all sponsor-backed loans within private credit are exposed to software alone. Some argue this feels similar to the lead-up to the 2008 financial crisis, while others argue the fears are overblown given the private credit market is a relatively small place in the larger global credit market and not a systemic situation. Markets have become so sensitive as of late that even a thought exercise published on Substack by a little-known research firm outlining a world devastated by the widespread use of AI had the power to sink stocks.

Moving forward, investors are starting off March with a slate of new risks to assess stemming from the escalating war with Iran. Following the initial attack, we have seen initial jumps in both gold and the U.S. dollar, both serving as a safe haven as investors take off risk. Global stock markets initially sold off when markets reopened following the weekend attacks and have since recovered some losses. The most notable reaction is with the spike in oil with the war effectively closing the Strait of Hormuz, which is responsible for carrying about one-fifth of the world’s oil. This upward pressure on oil prices has led to markets becoming concerned about further inflationary pressure and how that may impact the Fed. Bond yields have jumped across the yield curve and money markets are repricing expectations of the Fed’s next rate cut back to September from July.

Disruption is not new, and threats will come and go. As your advocate, JNBA continues to monitor the market environment diligently and is committed to keeping you informed. Diversification remains paramount to JNBA’s investment philosophy and for client portfolios to help isolate from fear-driven markets. Rather than reacting to short-term market headlines, our Investment Committee emphasizes disciplined, long-term decision-making to help clients stay focused and confident through market changes. We encourage you to reach out to your JNBA Advisory Team with any questions.

Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from JNBA Financial Advisors, LLC.

Please see important disclosure information at jnba.com/disclosure