When periods of weakness in the markets occur, it is vitally important for investors of long-term portfolios to “stay the course.” Here at JNBA Financial Advisors, we also believe there are steps that investors can take to potentially improve their long-term outcomes following periods of market weakness. To bridge the gap between long-term strategy and current market conditions, the JNBA Investment Committee makes tactical asset allocation decisions with the goal of enhancing return and mitigating risk characteristics. The main tactical lever we utilize is the broad asset allocation of stocks vs. fixed income/cash. We have built this strategy based on third-party models and our Investment Committee’s review of our client’s specific portfolio holdings. In practice, we multiply each portfolio’s allocation by approximately 10% of the total stock allocation and invest in either U.S. Large-Cap stocks or short-term fixed income, depending on the signal from the models that we utilize. For example, a 10% adjustment to a 60% stock/40% fixed income portfolio could result in a roughly 6% equity change to a client’s asset allocation based on the current environment, depending on the client’s unique portfolio and tax situation.

We recently mentioned that financial markets are in a sensitive spot amidst a backdrop of challenging economic and inflationary data, as well as the heightened vulnerability of companies susceptible to disruption from the advancement of AI technology. Now, we are seeing further uncertainty as the conflict escalates in Iran and across the Middle East, with volatility stemming from investors trying to determine how impactful this geopolitical shock could be for the global economy with many important variables still uncertain. To recognize this heightened uncertainty, JNBA’s Investment Committee is positioning portfolios more cautiously towards equities.

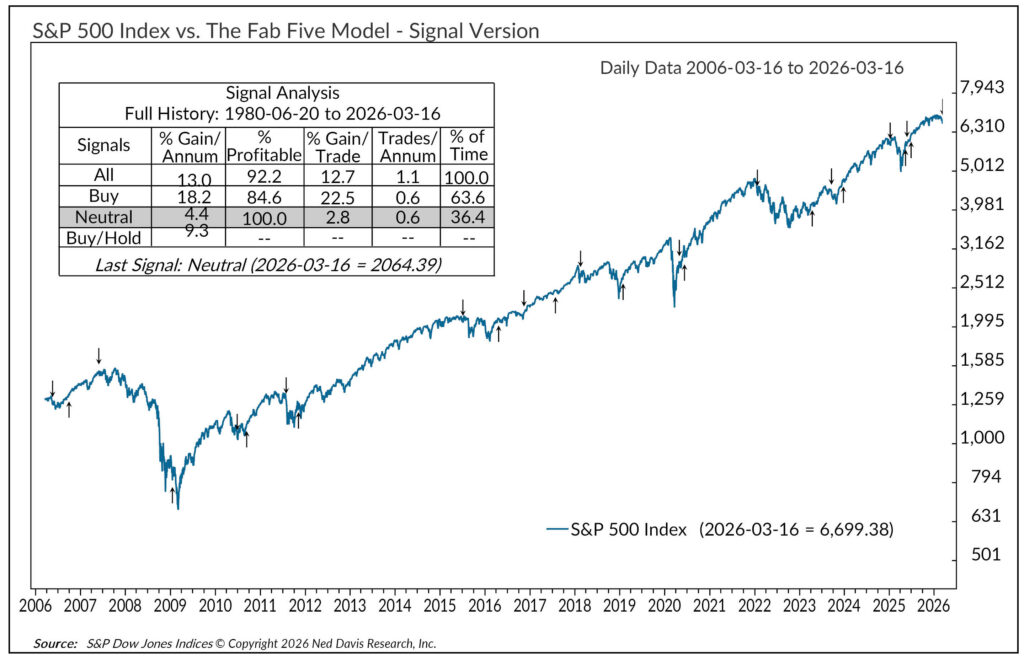

How often this shift is made is largely based on an external independent research provider, Ned Davis Research. They have developed a rigorous model based on economic and market data to determine when to be more or less exposed to the S&P 500 at various times. On average, the model typically shifts its recommendation 1.1 times per year, with recent shifts going underweight stocks in early 2025 ahead of the market selloff from the Trump Administration’s sweeping tariff announcements before shifting to overweight stocks as the market began to recover. While nothing is guaranteed, the model has a strong track record of yielding compelling performance results over time.

While our Investment Committee evaluates each data point in the context of the environment for the majority of its decision making, we believe the long-term track record of these tactical shifts provides strong alignment between our client portfolios and overall financial goals, with the foundation of our portfolios designed to meet the long-term financial life planning objectives of the individual client. We encourage you to reach out to your JNBA Advisory Team with any questions.

Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from JNBA Financial Advisors, LLC.

Please see important disclosure information at jnba.com/disclosure